Comfort Systems USA Stock 2026 Outlook: Buy the Data Center and HVAC Infrastructure Leader

Comfort Systems USA capitalises on AI infrastructure growth, showcasing strong earnings and backlog expansion.

NEW YORK — Comfort Systems USA Inc. (NYSE: FIX) has positioned itself as a major beneficiary of the artificial intelligence infrastructure boom and broader non-residential construction spending in 2026, delivering exceptional earnings growth and strong backlog expansion that support a bullish long-term outlook.

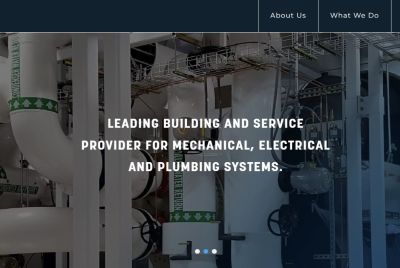

As of early June 2026, shares trade around $480 after a substantial year-to-date rally. The mechanical contractor and building services provider has been a standout performer, driven by surging demand for HVAC, electrical and plumbing systems in hyperscale data centers, semiconductor manufacturing facilities and other high-tech projects.

Comfort Systems reported robust first-quarter 2026 results, with revenue increasing significantly year-over-year and earnings per share beating expectations. The company highlighted strong backlog growth, particularly in data center and technology-related projects, as hyperscalers accelerate AI infrastructure buildouts. Management raised full-year guidance, citing sustained momentum in key end markets and operational efficiencies.

Analysts are overwhelmingly bullish. Multiple firms have raised price targets following recent earnings reports, with some reaching as high as $650. Consensus leans toward Strong Buy, with recent upgrades emphasizing Comfort Systems' exposure to secular growth trends in data centers and its proven execution capabilities.

The bullish case for buying Comfort Systems centers on its leadership in mechanical contracting for mission-critical facilities. As AI and cloud computing drive unprecedented demand for power, cooling and infrastructure, the company's expertise in designing and installing complex HVAC and related systems makes it a preferred partner for data center developers and general contractors. Its national footprint and established relationships provide a competitive advantage in securing large-scale projects.

Beyond data centers, Comfort Systems benefits from industrial manufacturing expansion, semiconductor plant construction and general commercial building activity. The company's diversified end-market exposure reduces reliance on any single sector while capitalizing on multiple growth drivers, including reshoring trends and energy efficiency initiatives.

Comfort Systems maintains a strong balance sheet with solid cash flow generation, supporting organic growth, strategic acquisitions and shareholder returns through dividends. The company has a track record of disciplined capital allocation and successful integration of acquired businesses, enhancing its service offerings and geographic reach.

Risks for potential buyers include valuation that has expanded with recent gains, potential cyclical slowdowns in construction spending and labor or supply chain constraints in a hot market. The stock's recent performance leaves limited margin for error if project delays or cost pressures emerge.

For sellers or those on the sidelines, near-term volatility tied to broader industrial and construction sector movements warrants caution. While fundamentals are strong, elevated multiples reflect high expectations that could lead to pullbacks on any softening in data center spending.

Investment decisions in 2026 hinge on several factors. Sustained AI infrastructure investment by hyperscalers supports a constructive view. Comfort Systems' exposure to traditional commercial and industrial markets provides additional diversification. Strong backlog and raised guidance reinforce confidence in near-term performance.

Broader market context favors infrastructure and industrial plays like Comfort Systems. Rising data center power and cooling demands create multi-year opportunities, while reshoring and manufacturing investments add tailwinds. However, investors must monitor interest rates, labor availability and potential economic slowdowns.

Analyst sentiment has improved with recent earnings strength and upward revisions. Institutional ownership remains healthy, reflecting confidence among sophisticated investors. The company's ability to deliver on ambitious targets while navigating supply and labor constraints will be key.

For growth-oriented investors comfortable with industrial cyclicality, selective buying on weakness may appeal. Conservative portfolios might prefer smaller positions or waiting for clearer confirmation of sustained data center demand. Diversification across infrastructure and industrial holdings can help manage company-specific risks.

Comfort Systems' long history of mechanical contracting excellence positions it well for evolving industry needs. From traditional HVAC installations to complex mission-critical systems for data centers, the company continues adapting while maintaining strong customer relationships and operational discipline.

As the year progresses, upcoming quarterly results, project updates and industry conferences will serve as important catalysts. Comfort Systems' execution on backlog conversion and ability to scale in a high-demand environment will be closely watched.

The company continues investing in talent, technology and safety initiatives to support growth. Its focus on employee development and operational excellence has been a key factor in its ability to handle increasingly complex projects.

For retail investors, Comfort Systems offers an accessible way to participate in the data center and industrial construction boom. Its business model benefits from secular trends in technology infrastructure and manufacturing reshoring, making it a compelling infrastructure play.

Monday's trading reflected continued positive sentiment but also highlighted the stock's sensitivity to broader market moves. The gain fits within the context of strong recent performance driven by data center tailwinds.

As a leading mechanical contractor, Comfort Systems plays a vital role in enabling the infrastructure that powers the modern digital economy. Its solutions support everything from data centers to advanced manufacturing facilities, contributing to technological progress and economic growth.

Investors evaluating Comfort Systems should conduct thorough due diligence, consider individual risk tolerance and maintain a long-term perspective. The company's track record of execution and value creation through industry cycles supports optimism for continued success in the data center and infrastructure boom.

Overall, Comfort Systems remains a compelling growth story with significant competitive advantages. While risks around valuation, labor and cyclical construction spending persist, its exposure to high-growth markets, strong backlog and operational excellence make it an attractive consideration for investors seeking participation in the critical infrastructure enabling AI and technological advancement.

© Copyright 2026 IBTimes AU. All rights reserved.

- Recommended For You