A new RBA index for economic uncertainty: nothing to fear but fear itself

A new monthly uncertainty index has been constructed by the Reserve Bank of Australia (RBA) to track the cost of different factors such as international events and government policy decisions on the economy.

Uncertainty is widely recognised as being a drag for the economy. Workers who become more uncertain about their future wages typically reduce what they buy to save for the future and face events like, say, a pay cut.

Entrepreneurs unsure about the economic environment, such as fiscal incentive or the availability of technology, reduce their investment and wait until the uncertainty dissolves. Research has found in spikes of uncertainty, in a given country, overall demand for goods falls, at least temporarily.

While these sorts of predictions are common among economists and policy makers, it’s a lot harder to quantify the impact of uncertainty. What is needed is a way to measure the consequences of events that cause shocks of uncertainty in the economy. Unfortunately, economic uncertainty is not directly observable.

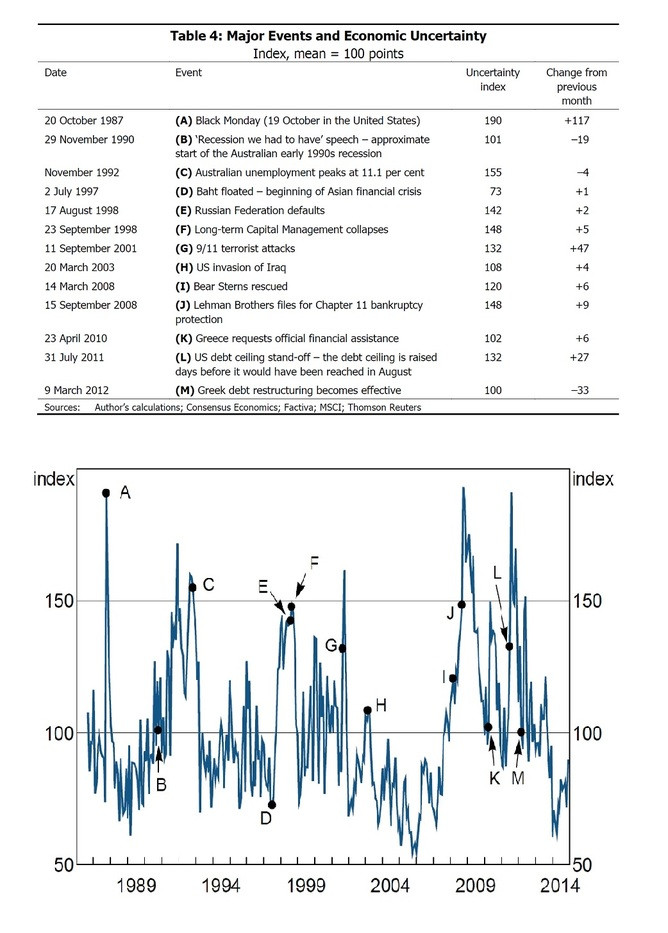

Economist Angus Moore from the RBA combined information from news (in particular, keywords such as “uncertainty”, “budget”, “policy” and so on), financial indicators (mainly, financial market volatility), and measures of disagreement among forecasters for key economic variables like firms' earnings and real GDP growth, to document the evolution of the Australian economic uncertainty from 1986 to 2014.

The RBA’s index appears to correlate with domestic events, like Paul Keating’s “recession we had to have” speech in November 1990, and even more clearly with external events such as the 9/11 terrorist attacks and Lehman Brothers' bankruptcy. Some events, as the Greek debt restructuring in March 2012, actually correspond to decreases in the index because they work in favour of reducing uncertainty.

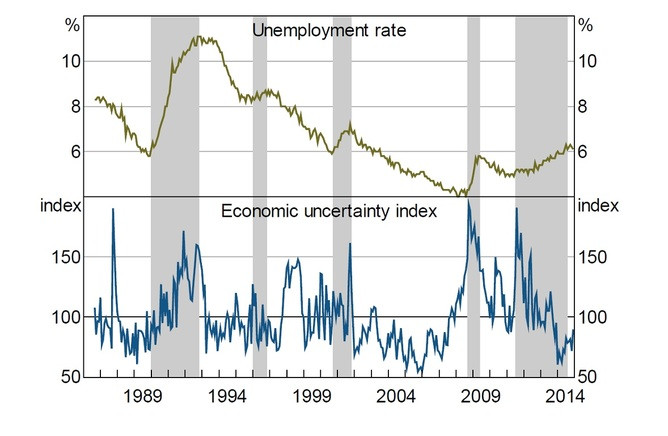

One test of this index is how is might relate to key macroeconomic indicators such as unemployment. If an increase in uncertainty is one of the reasons for slow growth, the labour market should show signs of slowdown in the presence of high uncertainty.

A comparison of the employment rate with the uncertainty index shows that economic uncertainty does seem to move hand-in-hand with unemployment in Australia. In particular, the economic uncertainty index is on average 20 points higher when unemployment is rising.

It may be that major external shocks - like 9/11 - may induce variations in the business cycle and, consequently, generate uncertainty. It’s difficult to factor in the business cycle in the data that used to create an uncertainty index.

The RBA’s model found that increases in uncertainty of a fairly modest amount - such as 30 basis points - are associated with a downturn characterised by lower employment growth, weaker retail sales growth, and a fall in consumer confidence.

However, the size of the impact appears to be small. Uncertainty shocks are found to have a noticeable effect on the level of the cash rate, which decreases by about 20 basis points. This may explain why the impact of uncertainty on real activity is modest, for example, the RBA would have promptly intervened when needed in order to tackle the effects of spikes in uncertainty.

Does this mean that uncertainty is unimportant? No. In fact, the results point to the fact that, in absence of an adequate systematic policy response by the RBA, uncertainty could have more markedly slowed down the Australian economy.

Olivier Blanchard, former chief economist of the International Monetary Fund, famously wrote in the aftermath of the collapse of the US financial markets in 2009 that there was “(nearly) nothing to fear but the fear itself.” Policymakers should aim at reducing uncertainty as much as possible by clearly communicating credible fiscal and monetary plans. This is crucial because, as the US case proves, economic uncertainty is more often than not driven by policy uncertainty.

In light of this relationship, Prime Minister Malcolm Turnbull should bear in mind that carefully managing Australian’s expectations on future economic policy reforms is a delicate task, and that backpedalling does not appear to be an option.

Efrem Castelnuovo, Principal Research Fellow, Melbourne Institute of Applied Economic and Social Research - Associate Professor, Faculty of Economics and Business, University of Melbourne

This article was originally published on The Conversation. Read the original article.

- MOST POPULAR IN Economy