Gold Price Dips Anew to a 3-Year Low of $1,180 an Ounce

The yellow metal continued its downward trend after the spot price of bullion hit a three-year low over the weekend to $1,180 an ounce. Since January 2013, gold price has retreated 29.5 per cent while the FTSE Gold Mines index of gold equities has declined 52 per cent.

The pace of the slide downward became faster after Federal Reserve Chairman Ben Bernanke announced the exit from its quantitative easing programme.

However, price of gold for immediate delivery increased 2.2 per cent to $1,227.05 at 3:05 p.m., Friday, New York time, its biggest gain since May 20. Gold future for August delivery also went up 1 per cent at $1,223.70 at the Comex in New York, and trading was 66 per cent higher the average the past 100 days.

The price of bullion dipped 27 per cent since January, making it the biggest yearly drop in price since 1981. Reckoned on a quarterly basis, it is set for the worst quarterly decline in almost 90 years.

Like gold, silver is also headed for its largest quarterly loss since 1980 as prices in New York settled at $19.47.

Marc Ground, a commodity strategist at Standard Bank in Johannesburg, however, told Bloomberg that there were some physical buying of gold and added if the trend continues, it would provide some support.

The support used to come mostly from Asian buyers, but the Indian government has tempered demand by restricting gold imports, while Chinese investors are waiting it out after they went on a buying spree in April, but saw prices drop further.

But few analysts are willing to forecast with confidence bottom prices of the yellow metal.

Kamal Naqvi, head of commodity investor sales at Credit Swiss, said, quoted by the Financial Times, "The key question is how low do we go? For the gold market it is typically to the next round number, but we have moved so quickly that's now people are forced to catch up ... It is currently a race to be the most bearish among the analysts."

-

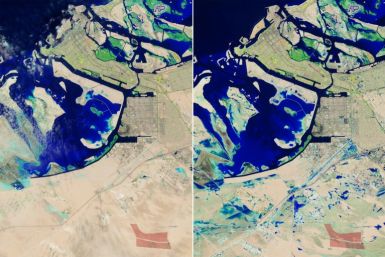

Oman, UAE Deluge 'Most Likely' Linked To Climate Change: Scientists

-

Macron Warns 'Mortal' Europe Needs Stronger Defence

-

Ahead Of Feared Rafah Invasion, Palestinians Mourn Bombardment Dead

-

Heatstroke Kills 30 In Thailand This Year As Southeast Asia Bakes

-

Portugal Marks 50 Years Of Democracy With Far Right On Rise